e-Banking Services Agreement

Effective as of 3/1/2021

Your use of Consumer e-Banking and Business e-Banking products and services offered by McHenry Savings Bank (“e-Banking Services”) is governed by this e-Banking Services Agreement (the “Agreement”), the Electronic Notice and Consent Agreement (the “e-Sign Consent”), the Terms and Conditions of Your Account, which may be found at https://www.mchenrysavings.com under the “Disclosures” tab at the bottom of the webpage (the “Deposit Terms and Conditions”), and any other terms and conditions we furnish to you in connection with any e-Banking Services that we may offer from time to time. As used in this Agreement, “us”, “we”, “our” and the term “Bank” mean McHenry Savings Bank, and “you” and “your” mean each Consumer or Business customer who has one or more Accounts at the Bank and utilizes e-Banking Services. This Agreement is between you and the Bank.

When you use or access, or permit any other person to use or access e-Banking Services or any other service offered by us, you agree to the terms and conditions of this Agreement. If the terms and conditions in this Agreement conflict with the terms and conditions of your Deposit Terms and Conditions as they apply to e-Banking Services, this Agreement controls. The terms and conditions of this Agreement are not intended to replace or modify any disclosures of other terms in your Deposit Terms and Conditions or other disclosures that are required by law to be provided by the Bank.

Through our Consumer e-Banking and Business e-Banking platforms, you may have access to several of your Accounts, including Deposit Accounts and Loan Accounts. Please refer to the underlying Deposit Terms and Conditions for each Account you access through the e-Banking Services for additional information about your rights and responsibilities, including those related to liability for unauthorized account use and statement errors created by federal law.

Certain capitalized terms have the meaning provided in Section IX of this Agreement. Capitalized terms not defined in this Agreement have the meaning provided in your Deposit Terms and Conditions.

ENROLLMENT.

At our option, we may permit you to request e-Banking Services by enrolling online for Personal Accounts or in person at any Bank location for Business Accounts in person. When you enroll, you authorize us to provide e-Banking Services to you in accordance with the terms and conditions of this Agreement and any terms and conditions we provide to you regarding additional services.

SET UP AND USE OF e-BANKING SERVICES.

ELIGIBILITY.

In order to activate e-Banking Services, you must have one or more Accounts with us. By activating e- Banking Services, you represent and warrant that you are eighteen (18) years of age or older and are authorized to enter into this Agreement. If the e-Banking Services will be provided in connection with a Business Account, you further represent and warrant that you are authorized by the Business to enter into this Agreement, to take action or make decisions on behalf of the Business, and to access the Business Account(s) through Business e-Banking. You must also complete authentication requirements imposed by the Bank from time to time and pay any fees described in the Fee Schedule and your Deposit Terms and Conditions.

ACCESS.

Our e-Banking Services generally are accessible twenty-four (24) hours a day, seven (7) days a week, except when e-Banking Services may be unavailable for any system maintenance or upgrade. We may modify, suspend, or terminate access to the e-Banking Services at any time and for any reason without notice.

EQUIPMENT AND SOFTWARE REQUIREMENTS.

To use our e-Banking Services, you need a computer and an Internet browser that meets our current minimum requirements, as set forth from time to time at Online Banking Software Compatibility. You are responsible for obtaining, installing, maintaining and operating all software and hardware or other equipment necessary for you to access and use our e-Banking Services, including but not limited to, an Internet service provider, current Internet browsers, commercially-reasonable encryption, anti-virus and Internet security software. You are responsible for any and all fees imposed by your Internet service provider and any associated communication service provider charges. By accepting these terms, you provide consent for the Bank to make periodic changes to its equipment and software requirements that do not materially change your ability to access or retain federally required disclosures.

ONLINE ACCOUNTS.

When you enroll in our e-Banking Services, you will have online access to your Accounts, which are reflected on our records as associated with the Social Security Number or Federal Tax Identification Number you provided at account opening. Not all e-Banking Services are available for all accounts offered by us or all customers using our e-Banking Services. If you open an additional Account at a later date or if you are added as a signer on an existing Account, you may have online access to your new Account within Consumer e- Banking or Business e-Banking. We may limit your access to our e-Banking Services at our sole discretion.

AUTHORIZED USERS – BUSINESS ACCOUNTS

This Section E applies only to Business Accounts in which an authorized representative will have access to and authority to use e-Banking Services and to take action or make decisions on behalf of a Business with respect to one or more Business Accounts. This includes a designated Business Administrator and any Authorized Users. In the event of a conflict with any provisions of this Agreement, the provisions of this Section E prevail. If you would like to give one or more Authorized Users online access to your Business Accounts(s) through Business e-Banking, you are required to do so through your Business Administrator, unless you are a sole proprietorship.

Access to Business e-Banking by your Business Administrator and/or any Authorized User(s) will continue until such time as you have given the Bank written notice of any changes to the Business Administrator and/or Authorized User(s) and until we have had a commercially reasonable time to act upon such notice. We may at our option and without liability to you, suspend access to the e-Banking Services by any Business Administrator and/or Authorized User at any time, without prior notice, if we deem it to be reasonably necessary under the circumstances to do so.

You ratify and confirm any and all actions and decisions of your Business Administrator and any Authorized User(s) appointed by your Business Administrator, regardless of whether or not such actions and decisions are within the scope of authority you granted to the Business Administrator and/or Authorized User(s). You are responsible for the administration, monitoring and control of any Business Administrator and Authorized User(s) in connection with their use of e-Banking Services on behalf of your Business.

All Businesses Other than Sole Proprietors.

If you have one or more Business Accounts, you may permit a Business Administrator and/or Authorized User to access and transact business on your Business Account(s) through the e-Banking Services. Business e-Banking is separate and distinct from your existing signature arrangements for your Business Accounts. As a result, when you appoint or designate a Business Administrator to access your Business Account(s) through Business e-Banking, or when your Business Administrator grants authority to an Authorized User to access your Business Accounts through Business e- Banking, the Business Administrator and/or Authorized User will have access to one or more Business Accounts that the Business Administrator and/or Authorized User may not otherwise have access based on existing signature arrangements.

You understand and agree that your Business Administrator is authorized to establish Security Credentials for any Authorized Users in connection with Business e-Banking. An Authorized User will have access to all Account Information and all documents and correspondence related to your Business Account(s). The Business Administrator is responsible for assigning, confirming, adding or deleting any Authorized Users. You hereby authorize your Business Administrator to receive and act upon all notices, documents and correspondence from us relating to Business e-Banking, including, without limitation, any changes, amendments or supplements to this Agreement. We recommend that as part of the enrollment in Business e-Banking, you elect to receive Alerts that will notify you when an Authorized User executes transactions in connection with your Business Account(s) through Business e-Banking. You are responsible for notifying us of any changes to your e-mail address, Mobile Device or telephone contacts to which Alerts are sent. You agree that the Bank shall not be liable to you for any unauthorized changes to an Authorized User, or for transactions executed by a Business Administrator or an Authorized User that could have been prevented by electing to receive an Alert or by maintaining appropriate contact information.

Sole Proprietors.

Access to your Business Account(s) through Business e-Banking is separate and distinct from your existing signature arrangements for your Business Account(s). As a result, when you give an Authorized User Security Credentials granting the authority to access and transact business on your Business Account(s) through Business e-Banking, the Authorized User will have access to one or more Business Accounts for which the Authorized User may not otherwise have access based on existing signature arrangements.

The e-Banking Services include the ability to establish Alerts that will notify you when an Authorized User executes transactions in connection with your Business Account(s) through Business e-Banking. Sole proprietors are required to utilize Alerts in connection with the e-Banking Services. You are responsible for notifying us of any changes to your e-mail address, Mobile Device or telephone contacts to which Alerts are sent. You agree that the Bank shall not be liable to you for any unauthorized changes to an Authorized User, or for transactions executed by an Authorized User that could have been prevented by electing to receive an Alert or by maintaining appropriate contact information.

E-BANKING SERVICES.

Services Offered.

This Agreement applies to the e-Banking Services you obtain through Consumer e-Banking or Business e-Banking. When you log on to use the e-Banking Services, this Agreement will appear as a link on the top right of the Business e-Banking web page or under the “Customer Service” navigation panel of the Consumer e-Banking web page.

When you complete the enrollment for Consumer e-Banking or Business e-Banking, you will receive Account Access, and to the extent applicable, Alerts for certain Account activity. You may need to separately enroll in other services that may be available now or in the future, including, but not limited to our Bill Pay Service, e-Statements Service, Mobile Banking Service, Mobile Check Deposit Service, Remote Deposit Capture Service, and Personal Finance Manager Service, and for Business customers, ACH services, wire transfers and enhanced reporting services.

Account Access. You can use Consumer e-Banking and Business e-Banking to: access your Account(s) and perform money transfers between your Accounts on either a one time or recurring basis; view certain Account Information, including balance and transaction information and Account statements; perform self-service Account maintenance; change Security Credentials; communicate with us via secure messaging from within Consumer e- Banking or Business e-Banking; and perform other activities.

Alerts. As part of your enrollment in Consumer e-Banking and Business e-Banking, you can elect to receive Alerts for certain types of Account activity. You are required to provide a valid phone number, e-mail address or other contact information for the recipient of the Alerts, and update us with any changes on an ongoing basis. Alerts are provided for your convenience and do not replace the need to carefully review your monthly Account statement(s). You understand Alerts may include personal or confidential information about you, such as your name, Account Information, and Account activity or status. Your receipt of each Alert may be delayed or impacted by factors not within our control, including delays or interruptions caused by your Internet service provider, phone carrier, or other parties. We will not be liable for (a) losses or damages arising from any non-delivery, delayed delivery, or misdirected delivery of the Alerts; (b) inaccurate content in the Alerts; or (c) any actions taken or not taken due to an Alert.

Bill Pay Service. If you enroll in the Bill Pay Service for Personal Accounts or Business Accounts, you can pay bills either on an automatic, recurring basis or periodically as you request. To enroll in the Bill Pay Service for Personal Accounts, click on the “Payments” tab in Consumer e-Banking to complete the enrollment process. To enroll in the Bill Pay Service for Business Accounts, contact a Customer Service Representative at Branch near you. When you enroll, you acknowledge that you have read and agree to the terms and conditions of this Agreement including the applicable terms and conditions for the Bill Pay Service in Section V.

Personal Finance Manager Service. If you enroll in Personal Finance Manager Service, you can view, organize and maintain information about your McHenry Savings Bank Account(s) as well as your non-McHenry Savings Bank accounts that you access through your computer or Mobile Device. To enroll in the Personal Finance Manager Service, click on the “Personal Finance” tab in Consume e-Banking to complete the enrollment. When you enroll, you acknowledge that you have read and agree to the terms and conditions of this Agreement including the terms and conditions governing the Personal Finance Manager Service in Section VI.

Third Party Account Information. You may use our e-Banking Services to retrieve your information maintained online by other financial institutions and merchants/billers, with which you have customer relationships, maintain accounts or engage in financial transactions and other log-in related information (“Third Party Account Information”). We do not review, verify or analyze the Third Party Account Information for accuracy or any other purpose. There may be technical difficulties which result in a failure to obtain data, a loss of data, a loss of personalized settings or other service interruptions. Third Party Account Information is timely only to the extent that it is promptly provided by the third-party sites. Third Party Account Information may be more up to date when obtained directly from the third-party sites. You are responsible for providing accurate and updated (as necessary) account numbers, user names, passwords and other log-in related information (“Registration Information”) so that you are able to access Third Party Account Information through our e-Banking Services. If you become aware of any unauthorized access to or use of your Third Party Account Information, you should notify your financial institution, merchant and/or biller immediately. By submitting data, passwords, user names, PINs, log-in information, materials and other information to us through Consumer e-Banking or Business e-Banking, you are licensing that content to us solely for the purpose of providing this service to you and for such other purposes as are set forth in the Privacy Policy under Subsection f) below (the “Privacy Policy”). You further represent that you are entitled to provide this information to us for purposes of this service and we are not required to pay any fees to any third parties for this information. We may use and store the content in accordance with the Privacy Policy. By using this service, you expressly authorize us to access your Third Party Account Information maintained by identified third parties, on your behalf as your agent. When you use the Add Accounts feature of our e-Banking Services, you will be directly connected to the website for the third party you have identified. We will submit information, including user names and passwords that you provide to log you into the site. You hereby authorize and permit us to use and store the information submitted by you (such as account passwords and user names) in order to provide this service, access Third Party Account Information maintained by third parties, and to configure this service so that it is compatible with the third-party sites for which you submit your information. You acknowledge and agree that when we are accessing and retrieving Third Party Account Information from the third-party sites, we are acting as your agent, and not as the agent of or on behalf of the third party. You understand and agree that this service is not sponsored or endorsed by any third parties providing Account Information or accessible through this service.

Privacy Policy. We will not sell or rent your personal information to anyone, for any reason, at any time. We use and disclose your personal information only as follows: (a) to analyze usage and improve our e-Banking Services, (b) to deliver to you any administrative notices, alerts and communications relevant to your use of our e-Banking Services, (c) to fulfill your requests for certain products and services, (d) for market research, project planning, troubleshooting problems, detecting and protecting against error, fraud or other criminal activity, and (e) in order to enable us to offer additional product offerings to you. Notwithstanding the foregoing, we reserve the right (and you authorize us) to share or disclose your personal information when we determine, in our sole discretion, that the disclosure of such information is necessary or appropriate (x) to enforce our rights against you or in connection with a breach by you of this Agreement, (y) to prevent prohibited or illegal activities, or (z) when required by any applicable law, rule regulation, subpoena or other legal process.

E-Statements Service. We will provide certain Account Information electronically, including Account statements for your Account(s), through Consumer e-Banking and Business e- Banking. If you want to receive statements only in electronic form, (“e-Statements”), you must enroll in the e-Statements Service. For Personal Accounts, you may enroll in the e-Statements Service by either clicking the “Account” button located on the e-Statements page accessible through the Accounts tab, or click the “Preferences” link in the header or footer of the page and select Statement Preferences. When you enroll, you acknowledge that you have read and agree to the terms and conditions of this Agreement and the Consumer e-Banking and Business e- Banking Electronic Communications Delivery Notice and Agreement provided to you during your enrollment. For Business Accounts, contact a Customer Service Representative to receive e-Statements through Business e-Banking.

Service Changes. We may, from time to time, modify any e-Banking Service to include additional Accounts in Consumer e-Banking and Business e-Banking, introduce new e-Banking Services to Consumer e-Banking and Business e-Banking or new features to existing e-Banking Services, or modify or delete existing e-Banking Services or features in our sole discretion. By using any new or modified e-Banking Services or features when they become available, or if you permit any other person or entity to use or access the e-Banking Service, you agree to be bound by these or any revised terms and conditions concerning these e-Banking Services or features.

FEES.

You may incur fees if you use certain e-Banking Services available through Consumer e-Banking and Business. Please review the Fee Schedule we provide to you when you enroll or use each e-Banking Service, as applicable. You authorize us to debit your Account for all fees when incurred. In addition, other charges such as, Internet service provider fees, communication charges and the purchase of financial management software (if any) are your responsibility. We reserve the right to add or modify fees from time to time and will notify you when we do so.

TRANSFERS.

Description of Service. Through our transfer service, you may transfer funds internally between eligible Transaction Accounts that you maintain at the Bank, or externally between an eligible Transaction Account that you maintain at the Bank and an eligible Transaction Account at another financial institutions. Internal or external transfers can be made on a one-time basis or recurring in a predetermined amount. Transfers can be scheduled immediately or at a future date.

Eligibility. You must have at least two (2) eligible Transaction Accounts in order to transfer funds. You must register and we must approve, in accordance with our then-current verification procedures, each Transaction Account to or from which transfers may be initiated. When you register a Transaction Account, you represent that (a) you are the sole owner or a joint owner of the Transaction Account and or that you have all necessary legal rights and authority to transfer funds to or from the Transaction Account; and (b) the Transaction Account is located in the United States. If you are a joint owner of the Transaction Account, you further represent that: (i) you have been authorized by all of the other joint owners to operate such Transaction Account without their consent; and (ii) we may act on your instructions regarding the Transaction Account without liability to such other joint owner(s).

Limitations. Transfer amounts are limited to your available balance in your Transaction Account plus the available credit in any linked overdraft line of credit account. You authorize us to debit your Transaction Account for funds transfers you initiate through Consumer e-Banking or Business e- Banking. We are not required to transfer funds unless there are sufficient available funds in your Transaction Account (or available credit) on the transfer date. If there are insufficient available funds (or available credit), we may, but are not obligated to retry the transfer at a later date. Transfers are subject to any limitations on the number of transactions that apply to your Transaction Account(s) as provided in your Deposit Terms and Conditions. For security reasons, we may establish daily, per transaction, or other limitations on the amount of transfers in our discretion. These limits are subject to change from time to time upon notice to you at the extent required by applicable law. Business Administrators for Business Accounts may limit the daily and per transaction amount for internal transfers for any Account by each Authorized User.

Processing of Transfer Requests.

You must give us instructions in the content and formatting standards that we may require from time to time, in order to request, schedule, process, and settle the transfer. You are solely responsible for ensuring the accuracy of any information that you provide in your transfer instructions, identifying any errors contained in your instructions, and informing us as soon as possible if you become aware of any such errors. We are not under any obligation to complete a request for a transfer until such time as we obtain all information required to process the instruction in accordance with the terms and conditions of this Agreement.

As you may determine in your instructions, your instruction will either authorize us to debit your Transaction Account and send funds on your behalf to the other Transaction Account designated by you; or, as applicable, to credit your Transaction Account when we receive funds from the other Transaction Account designated by you. You also authorize us to reverse a debit if the debit is returned for any reason; or a credit if the remittance is not honored by us for any reason.

Transfers can be made on a one-time or recurring basis. One-time transfers may be immediate or scheduled for a future date. The recurring transfer feature may be used when a set amount is transferred at regular intervals. You agree that you will maintain sufficient available funds or available credit on the date each transfer is scheduled to occur.

At the time you schedule a transfer, we will provide you with the amount of funds available. All transfer requests received before the cut-off time will be processed on the Business Day the transfer is scheduled to occur, and any transfer requests received after the cut-off time will be processed on the next Business Day.

When you make a transfer from an Account, the options to send the funds that are available to you will display in Consumer e-Banking or Business e-Banking, as applicable. One or more options may be available to you. Each option will include the estimated time of processing of the funds from your Account. Funds received from a transfer will not be available to you until we actually receive the funds from the other Transaction Account. Estimated times that we provide in online banking are subject to change. You acknowledge and agree that, due to circumstances beyond our control and/or in accordance with the provisions of this Agreement, transfers may be processed after the estimated dates, and we will only be liable for late transfers only to extent set forth herein and under applicable law. Funds requested to be transferred will be debited or credited to an external Transaction Account according to the receiving financial Institution’s availability and transaction processing schedule.

Changes to Transfers. Request for immediate transfers of funds cannot be cancelled. You may cancel or modify a transfer scheduled for a future date, including a recurring transfer. Once we have started processing a transfer, it cannot be cancelled or modified. Before such time, we may make reasonable attempts to return any unclaimed, refused, refunded, prohibited or denied transfer to your Transaction Account or to stop or recover a transfer that was initiated, processed, or settled erroneously, but we do not guarantee such recovery and will bear no responsibility or liability resulting from our failure to do so or incorrect information entered by you in your instructions, to the extent permitted by applicable law.

Refused Transfers. We reserve the right to refuse any transfer for any reason, including instances where there are not sufficient available funds in your Transaction Account to cover the transfer or we, in good faith, believe the transfer may be fraudulent, erroneous, illegal, in violation of this Agreement or the Deposit Terms and Conditions, or suspicious. To the extent required by law, we will notify you promptly if we decide to refuse a transfer. The notification is not required if you attempt to make a transfer that is not allowed under the Agreement.

Returned Transfers. You understand and agree that transfers may be returned for various reasons such as errors contained in your instructions. We may attempt to research the cause of a returned transfer and notify you to resend the transfer with the corrected information.

Liability. We are not liable if we are unable to complete any internal or external transfers request that you initiate if: (1) through no fault of ours, the eligible Transaction Account does not contain sufficient funds to complete the transfer on the scheduled transfer date; (2) we notified you or you otherwise knew that the transfer service was not working properly before we initiated the transfer; (3) we refused the transfer as described in section 6 above; (4) you have not provided us with correct information, such as the correct eligible Transaction Account or account information; and/ or (5) circumstances beyond our control prevent the proper execution of the transfer.

SECURITY CREDENTIALS.

You hereby agree that we are authorized and entitled to act on transaction and other instructions received using your Security Credentials, and you agree that the use of your Security Credentials will have the same effect as your signature authorizing the transaction(s) to the fullest extent permitted by law. If you disclose your Security Credentials to any person or entity, including any data aggregation service provider, direct us to assign Security Credentials to any entity or person, or permit any other person or entity to access or use Consumer e-Banking or Business e-Banking, you are responsible for any activity and transactions performed from your Account(s) by such person or entity and for any use of your personal information and Account Information by such person or entity. The loss, theft or unauthorized use of your Security Credentials could cause you to lose some or all of the money in your Account(s), plus any amount available under any line of credit. It could also permit unauthorized persons to have access to your personal information and Account Information and to use the information for fraudulent purposes including identity theft.

You are responsible for maintaining the security of your Security Credentials and for any financial transactions performed or information received using such Security Credentials to the fullest extent allowed by law.

We will ask for your Security Credentials to confirm your identity only when you log on to Consumer e- Banking and Business e-Banking, or if you call us. We will never contact you via e-mail, secure messaging from within Consumer e-Banking or Business e-Banking or telephone requesting your Security Credentials. If you are ever contacted by anyone asking for your Security Credentials, you should refuse and immediately contact us. You may be the target of attempted identity theft.

ADDRESS OR OTHER CHANGES.

It is your responsibility to ensure that your contact information with the Bank is current and accurate. This includes, but is not limited your mailing address, primary and/or cell phone numbers and your email address. Individuals (not Businesses) may request address changes through Consumer e-Banking. Businesses may request address changes by contacting a Customer Service Representative at 1-815-385-3000.

REPORTING UNAUTHORIZED ACCOUNT ACCESS.

If you believe someone may attempt to use or has used Consumer e-Banking or Business e-Banking to access your Accounts or your Account Information without your permission, or that any other unauthorized use or security breach has occurred, you agree to immediately notify us at 1-815-385-3000. You may also contact us electronically by sending a secure message through Consumer e-Banking or Business e-Banking, or by writing to us at: McHenry Savings Bank, 353 Bank Dr., McHenry, IL. 60050. To report potential errors, such as unauthorized transactions or statement errors, please refer to the procedures described in your Deposit Terms and Conditions.

INDEMNITY.

You acknowledge and agree that you are personally responsible for your use of e-Banking Services and agree, to the fullest extent permitted by applicable law, and except as set forth in this Agreement, the Deposit Terms and Conditions, and any other terms and conditions applicable to your Account(s), to indemnify and hold us and our officers, directors, employees and agents harmless from and against any loss, damage, liability, cost or expense of any kind, including reasonable attorneys’ fees that we may incur in connection with a third party claim or otherwise related to your use of e-Banking Services, the use of e-Banking Services by anyone using your Security Credentials or the Security Credentials you have assigned to someone else, or your violation of this Agreement or the rights of any third party. Your obligations under this section survive termination of this Agreement.

LIMITATIONS ON OUR LIABILITY.

Access.

In the event of a system failure or interruption, your data may be lost or destroyed. Any transaction that you initiated, were in the process of completing, or completed shortly before system failure or interruption should be verified by you through means other than Consumer e-Banking and Business e-Banking to ensure the accuracy and completeness of such transaction.

You assume the risk of loss of your data during any system failure or interruption and the responsibility to verify the accuracy and completeness of any transaction affected by the system failure or interruption. We will not be liable for failure to provide access or for interruptions in access to Consumer e-Banking and Business e-Banking due to a system failure or due to other acts or circumstances beyond our control.

Your Systems Including Computer Equipment and Software.

You acknowledge that there are certain security, corruption, transmission error and access availability risks associated with using open networks such as the Internet and you hereby expressly assume such risks.

We are not responsible for any error, problem, damages or other loss you may suffer due to malfunction or misapplication of your systems, including your Internet service provider, your personal financial management or other software, or any equipment you may use (including your telecommunications facilities and computer hardware) to access or communicate with Consumer e- Banking and Business e-Banking.

TERMINATION.

We can terminate your access to Consumer e-Banking or Business e-Banking or any e-Banking Service under this Agreement at any time without notice to you for any reason. You may terminate your access to Consumer e-Banking, Business e-Banking or any e-Banking Service at any time by contacting us. In the event of any such termination, all unprocessed transfers will be canceled and all Scheduled Payments through the Bill Pay Service for all Accounts will be cancelled. You must make other arrangements to make these payments. If you voluntarily terminate your access to Consumer e-Banking or Business e-Banking or any e-Banking Service, you will need to re-enroll in Consumer e-Banking or Business e-Banking, or the respective e-Banking Service, as applicable.

CHANGE IN TERMS AND OTHER AMENDMENTS.

We may add, delete, or amend terms, conditions and other provisions, fees, charges, or other terms described in this Agreement, the Fee Schedule and the terms and conditions of any e-Banking Service you use. We will send written notice to you if required by applicable law. You agree that all notices or other communications we are required to provide to you may be sent to you electronically through an e-mail message, or by posting changed terms on our Consumer e-Banking and Business e-Banking website, or by regular mail. Please access and review this website regularly. If you continue using any e-Banking Service after the effective date of the notice, you are bound by any such change to this Agreement.

TERMS AND CONDITIONS OF YOUR ACCOUNTS.

In addition to this Agreement, you agree to be bound by such other terms and conditions we furnish to you in connection with Consumer e-Banking and Business e-Banking and the e-Banking Services which you access using Consumer e-Banking and Business e-Banking. When you add an Account to Consumer e-Banking and Business e-Banking, this does not change the Deposit Terms and Conditions that already apply to your Account. You should review the Deposit Terms and Conditions for applicable fees, funds availability policies, limitations on the numbers of transactions and other restrictions that may limit your use.

In the event of a direct conflict between the terms of this Agreement, any other terms and conditions we furnish to you in connection with any e-Banking Services, and your Deposit Terms and Conditions, unless specifically set forth in the other terms and conditions we furnish to you in connection with any e-Banking Services, the order of priority is as follows: (i) this Agreement; (ii) the other terms and conditions we furnish to you in connection with the e-Banking Services, as applicable; and (iii) the Deposit Terms and Conditions.

You acknowledge and agree that we may rely on any authorized signatures as provided by you for your Deposit Terms and Conditions. You further acknowledge and agree that in the event we have no signature card on file for you that we are authorized to rely and act on any signature we have on file for you (such as on a check) and if there is no signature on file that we in our sole discretion may (i) pay any transaction or Item or (ii) return any transaction or Item without honoring it, without liability.

RECORDS.

Our records kept in the regular course of business will be presumed to accurately reflect the contents of your instructions to us and, in the absence of manifest error, will be binding and conclusive. Consumer e-Banking and Business e-Banking information is generally updated regularly, but is subject to adjustment and correction and therefore should not be relied upon by you for taking, or forbearing to take any action. Account Information provided to you as part of Consumer e-Banking and Business e-Banking is not the official record of your Account or its activity.

ELECTRONIC NOTICE.

You may use e-mail through our secure messaging system located within Consumer e-Banking and Business e-Banking to contact us about inquiries, maintenance and/or certain problem resolution issues. Regular e-mail may not be a secure method of communication; therefore we recommend you do not contact us by regular e- mail. There may be times when you need to speak with someone immediately (especially to report a lost or stolen Security Credentials). In those cases, do not use e-mail. Instead, please call us at 1-815-385-3000.

In the e-Sign Consent provided to you as part of your enrollment in Consumer e-Banking and Business e- Banking, you agree that the Agreement and all Notices (both as defined in the e-Sign Consent) may be provided to you electronically rather than in paper form. Please refer to your copy of the e-Sign Consent for additional information on withdrawing your consent or requesting paper copies of the Agreement and any Notices.

HOURS OF OPERATION.

Our representatives are available to assist you Monday through Thursday 9:00 a.m. to 5:00 p.m., Friday 9:00

a.m. to 6:00 p.m. and Saturday 9:00 a.m. to 1:00 p.m. by telephone at 1-815-385-3000 or through our secure messaging system located within Consumer e-Banking and Business e-Banking.

OWNERSHIP OF WEBSITE.

The content, information and offers on our website are copyrighted by or used by license by the Bank and the unauthorized use, reproduction, linking or distribution of any portion is strictly prohibited. We grant to you, for your personal or internal business purposes only, a nonexclusive, limited and revocable right to access and use Consumer e-Banking and Business e-Banking. You agree not to use Consumer e-Banking and Business e-Banking for any other purpose, including commercial purposes such as co-branding, linking or reselling, without our prior written consent.

Our websites are located in the United States, may be owned, hosted or controlled by us, our affiliates or a third party selected by us, and may also be used for other Internet Services offered by us or any of our affiliates. We make no representation or warranty that our website or Consumer e- Banking and Business e-Banking are available or appropriate for use in countries other than the United States. You are responsible for complying with all laws (including foreign and domestic laws and regulations requiring governmental consent) applicable to where you use Consumer e-Banking and Business e-Banking or view the website.

WEB SITE LINKS.

The website may contain links to other third party websites. When linking to those third party sites you are subject to the terms, including the privacy policy, posted by those third party sites. We are not responsible for, nor do we control, the content, products, or services provided by linked websites. We do not endorse or guarantee the products, information, services or recommendations provided by linked sites and are not liable for any failure of products or services advertised on those websites. In addition, each third party website may provide less security than we do and have a privacy policy different than ours. You should review such third party website’s security and privacy policy to understand your rights. Your access, use and reliance upon such content, products or services are at your own risk.

GOVERNING LAW.

This Agreement is governed by and construed in accordance with federal law and the laws of Illinois, without regard to Illinois conflict of law provisions. You consent to the jurisdiction of the state and federal courts of Illinois and agree that any legal action or proceeding with respect to the Agreement will be commenced in such courts.

SCOPE OF AGREEMENT.

This Agreement represents our complete agreement with you relating to your access to and use of e-Banking Services through Consumer e-Banking and Business e-Banking. No other statement, oral or written including language contained in our website, unless otherwise expressly noted herein, is part of this Agreement.

PARTIES’ RESPONSIBILITIES - PROVISIONS APPLICABLE TO CONSUMER ACCOUNTS ONLY.

JOINT ACCOUNTS.

If your Account is opened in the names of, and owned by, two or more individuals, and the word “or” separates the names of the Account owners, we may act on the instructions of any Account owner (joint tenancy with rights of survivorship). If the word “and” separates the names of the Account owners, we will not act on your instructions unless all signatures have been obtained (tenancy-in-common).

LIMITATIONS ON BANK'S LIABILITY.

THE BANK, INCLUDING OUR AFFILIATES AND AGENTS, ARE NOT RESPONSIBLE FOR ANY LOSS, DAMAGE OR INJURY OR FOR ANY DIRECT, INDIRECT, SPECIAL, INCIDENTAL, PUNITIVE, EXEMPLARY, OR CONSEQUENTIAL DAMAGES, INCLUDING LOST PROFITS, ARISING FROM OR RELATED TO THE EQUIPMENT, BROWSER AND/OR THE INSTALLATION OR MAINTENANCE THEREOF, ACCESS TO OR USE OF CONSUMER e-Banking, FAILURE OF ELECTRONIC OR MECHANICAL EQUIPMENT OR COMMUNICATION LINES, TELEPHONE OR OTHER INTERCONNECT PROBLEMS, OR INCOMPATIBILITY OF COMPUTER HARDWARE OR SOFTWARE, FAILURE OR UNAVAILABILITY OF INTERNET ACCESS, PROBLEMS WITH INTERNET SERVICE PROVIDERS, PROBLEMS OR DELAYS WITH INTERMEDIATE COMPUTER OR COMMUNICATIONS NETWORKS OR FACILITIES PROBLEMS WITH DATA TRANSMISSION FACILITIES OR ANY OTHER PROBLEMS YOU EXPERIENCE DUE TO CAUSES BEYOND OUR CONTROL. EXCEPT AS OTHERWISE EXPRESSLY PROVIDED IN ANY APPLICABLE AGREEMENT, YOU UNDERSTAND AND AGREE THAT YOUR USE OF CONSUMER e-Banking IS AT YOUR SOLE RISK AND THAT CONSUMER e-Banking AND ALL INFORMATION, SERVICES, PRODUCTS AND OTHER CONTENT (INCLUDING THIRD PARTY INFORMATION, PRODUCTS AND CONTENT) INCLUDED IN OR ACCESSIBLE FROM ANY WEBSITE, IS PROVIDED ON AN AS IS BASIS, AND IS SUBJECT TO CHANGE AT ANY TIME. YOU ACKNOWLEDGE THAT WE MAKE NO WARRANTY THAT CONSUMER e-Banking WILL BE UNINTERRUPTED, TIMELY, SECURE OR ERROR-FREE. TO THE FULLEST EXTENT PERMITTED BY LAW, WE, INCLUDING OUR AFFILIATES AND AGENTS, DISCLAIM ALL REPRESENTATIONS, WARRANTIES AND CONDITIONS OF ANY KIND (EXPRESS, IMPLIED, STATUTORY OR OTHERWISE, INCLUDING BUT NOT LIMITED TO THE WARRANTIES OF MERCHANTABILITY AND FITNESS FOR A PARTICULAR PURPOSE, TITLE, AND NON- INFRINGEMENT OF PROPRIETARY RIGHTS) AS TO CONSUMER e-Banking AND ALL INFORMATION, SERVICES AND OTHER CONTENT (INCLUDING THIRD PARTY INFORMATION, PRODUCTS AND CONTENT) INCLUDED IN OR ACCESSIBLE FROM THE WEBSITE.

CONSUMER LIABILITY FOR UNAUTHORIZED TRANSACTIONS.

If you are a Consumer customer and use Consumer e-Banking to make transfers or use the Bill Pay Services for your Deposit Account(s), the procedures for handling unauthorized transactions, your liability for such transactions, and your rights and liability with respect to the Bank’s failure or delay in making transfers or stopping payment are set forth in your Deposit Terms and Conditions.

Consumer e-Banking may allow you to access one or more Loan Accounts with the Bank. With open-end Loan Accounts, you may be liable for the unauthorized use of your Loan Account. Please refer to your Loan Terms and Conditions of Your Account for further information.

Please call us AT ONCE at 1-815-385-3000 if you believe your Security Credentials have been lost or stolen. Telephoning is the best way to minimize your losses.

RESOLVING ERRORS OR PROBLEMS.

If you think your Deposit Account statement is wrong or if you need more information about a transfer listed on the statement, contact us by telephone at 1-815-385-3000, contact us electronically by sending a secure message through Consumer e-Banking or Business e-Banking our secure messaging system, or write us at McHenry Savings Bank, 353 Bank Dr., McHenry, IL. 60050 as soon as you can.

If you think there is an error on your Loan Account statement, please refer to your Loan Electronic Fund Transfers Your Rights and Responsibilities for the procedures for notifying us. Please note that if you do not notify us in writing we may not be required to investigate any potential errors.

PARTIES’ RESPONSIBILITIES - PROVISIONS APPLICABLE TO BUSINESS ACCOUNTS ONLY.

ACKNOWLEDGEMENT OF COMMERCIALLY REASONABLE SECURITY PROCEDURES.

By using Business e-Banking, you acknowledge and agree that this Agreement sets forth security procedures for electronic banking transactions which are commercially reasonable. You agree to be bound by any action taken by us upon our receipt of any instruction received using your Security Credentials.

LIMITATION OF BANK'S LIABILITY FOR BUSINESS CUSTOMERS ONLY.

THE BANK WILL HAVE NO LIABILITY TO YOU FOR ANY UNAUTHORIZED TRANSACTION MADE USING YOUR SECURITY CREDENTIALS THAT OCCURS BEFORE YOU HAVE NOTIFIED US OF POSSIBLE UNAUTHORIZED USE AND WE HAVE HAD REASONABLE OPPORTUNITY TO ACT ON THAT NOTICE. YOU ASSUME THE ENTIRE RISK FOR THE FRAUDULENT, UNAUTHORIZED OR OTHERWISE IMPROPER USE OF YOUR SECURITY CREDENTIALS. WE ARE ENTITLED TO RELY ON THE GENUINENESS AND AUTHORITY OF ALL INSTRUCTIONS RECEIVED BY US WHEN ACCOMPANIED BY REQUIRED SECURITY CREDENTIALS, AND TO ACT ON SUCH INSTRUCTIONS. If we fail or delay in making a transaction, pursuant to your instructions, or if we make a transaction in an erroneous amount which is less than the amount per your instructions, unless otherwise required by law, our liability is limited to interest on the amount which we failed to timely transaction, calculated from the date on which the transaction was to be made until the date it was actually made or you canceled the instructions. We may pay such interest either to you or the intended recipient of the transaction, but in no event will we be liable to both parties, and our interest payment to either party will fully discharge any obligation to the other. If we make a transaction in an erroneous amount which exceeds the amount per your instructions, or if we permit an unauthorized transaction after we have had a reasonable time to act on a notice from you of possible unauthorized use as described above, unless otherwise required by law, our liability will be limited to a refund of the amount erroneously paid or transferred, plus interest thereon from the date of the transaction to the date of the refund, but in no event to exceed thirty (30) days’ interest. If we become liable to you for interest compensation under this Agreement or applicable law, such interest will be calculated based on the average federal funds rate at the Federal Reserve Bank in the district where the Bank is headquartered for each day interest is due, computed on the basis of a 360-day year. UNLESS OTHERWISE REQUIRED BY LAW, IN NO EVENT WILL THE BANK BE LIABLE TO YOU FOR SPECIAL, INDIRECT OR CONSEQUENTIAL DAMAGES INCLUDING, WITHOUT LIMITATION, LOST PROFITS OR ATTORNEYS’ FEES, EVEN IF WE ARE ADVISED IN ADVANCE OF THE POSSIBILITY OF SUCH DAMAGES.

Without regard to care or lack of care of either you or us, a failure to report to us any unauthorized transaction or error from any of your Business Accounts within thirty (30) days of our providing or making available to you a bank statement showing an unauthorized transaction or error will relieve us of any liability for any losses sustained after the expiration of such thirty-day (30-day) period and you will thereafter be precluded from asserting any such claim or error.

ERRORS AND QUESTIONS.

In case of any questions about Business e-Banking or your Business Accounts contact us by calling us at 1- 815-385-3000, contact us electronically by sending a secure message through Consumer e-Banking or Business e-Banking, or write us at McHenry Savings Bank, 353 Bank Dr., McHenry, IL. 60050 as soon as you can.

If you have questions about electronic transaction or payments or if you think that your statement is wrong or you need more information about a transfer listed on the statement, contact us immediately by telephone, electronically or in writing as specified above. We must hear from you no later than sixty (60) days after we provided or otherwise made available to you the FIRST statement on which the problem or error appeared. Failure to so notify us will preclude you from being able to assert a claim based on such problem or error. Any errors reported to us will be investigated by us and we will advise you of the results of our investigation.

BILL PAY SERVICES FOR PERSONAL ACCOUNTS AND BUSINESS ACCOUNTS.

These terms and conditions govern your use of our Bill Pay Services for Personal Accounts and/or Business Accounts, as applicable, which permit Consumer and Business customers to pay or designate Billers to receive a Bill Payment based on Payment Instructions provided by you.

PAYMENT SCHEDULING.

You may schedule two (2) types of payments to your Billers: One Time Payments or Recurring Payments. The earliest possible Scheduled Payment Date for each Biller will be designated within the Bill Pay Service when you are scheduling the payment. Therefore, the Bill Pay Service will not permit you to select a Scheduled Payment Date earlier than the earliest possible Scheduled Payment Date designated for each Biller. When scheduling payments, you must select a Scheduled Payment Date that is no later than the actual Due Date reflected on your Biller statement however, if the actual Due Date falls on a non-Business Day, you must select a Scheduled Payment Date that is at least one (1) Business Day before the actual Due Date.

PAYMENT REMITTANCE.

The cut-off time for Payment Instructions is provided within the Bill Pay Service. Payment Instructions received after the cut-off time on a Business Day or on a non- Business Day will be processed the next Business Day.

PAYMENT METHODS.

Payments will be made using the ACH, by paper check, or any other method chosen by us. You agree that we have the sole right to select the method in which to remit funds on your behalf to your Biller (each a Payment Method and collectively, Payment Methods). Your payment confirmation will list the Payment Method for each Bill Payment.

LIMITATIONS ON PAYMENTS.

The current maximum amount of any single payment is $10,000 and the aggregate maximum total amount of all payments processed on any Business Day is $25,000. If a transaction would exceed these amounts, a notice will be separately displayed at the time you submit your Payment Instruction. There are no minimum amounts which apply to a payment. These limits are subject to change from time to time.

PAYMENT CANCELLATION REQUESTS.

Except as otherwise provided in this Section F below, you may cancel or edit any Scheduled Payment (including Recurring Payments) by following the directions within the Bill Pay Service. There is no additional charge for canceling or editing a Scheduled Payment. Once we have begun processing a payment, it cannot be cancelled or edited online through the Bill Pay Service.

STOP PAYMENT REQUESTS.

Your ability to stop payment of a Scheduled Payment that has been, or is being, processed will depend on the Payment Method and whether your Account is a Personal Account or a Business Account. For Business Accounts, we must have a reasonable opportunity to act on any stop payment request. For Personal Accounts, you should submit stop payment requests in accordance with the applicable terms in your Deposit Terms and Conditions. To stop any Scheduled Payment that has been, or is being, processed, you must contact Customer Service to submit a stop payment request. If your Bill Payment Account is a Personal Account and the Payment Method is a paper check or electronic funds transfer, you may request a stop payment in accordance with the applicable provisions of your Deposit Terms and Conditions. For all other Payment Methods, although we will make every effort to accommodate your stop payment request, we are not liable to you for failing to do so. You may also be required to present your stop payment request in writing within fourteen (14) days. The fee for each stop payment request will be the current fee for such stop payment as set out in the Fee Schedule that applies to your account with Bill Pay rights.

PROHIBITED PAYMENTS.

You may make payments to Billers within the United States, subject to any maximum payment limits. You agree not to use the Bill Pay Service for payments made pursuant to court orders, fines, payments for gambling debts, or payments otherwise prohibited by law. In no event will we be liable for any claims or damages resulting from you scheduling these types of payments. We have no obligation to research or resolve any claim resulting from a prohibited payment. All research and resolution for any misapplied, misposted or misdirected payments will be solely your responsibility and not our responsibility.

ELECTRONIC BILL DELIVERY AND PRESENTMENT (E-BILLS).

This feature is for the presentment of electronic bills only. It is your sole responsibility to contact your Billers directly if you do not receive your bills. This electronic bill delivery feature does not alter your liability or the obligations that currently exist between you and your Billers. In addition, if you elect to activate one of the Bill Pay Service’s electronic bill options, you also agree to the following:

We are unable to update or change your personal information with the Biller such as, but not limited to, your name, address, phone numbers and e-mail addresses. You must contact the Biller directly to make any changes. Additionally, it is your responsibility to maintain all usernames and passwords for all Biller websites. You also agree not to use someone else’s information to gain unauthorized access to another person’s bill. We may, at the request of the Biller, provide to the Biller your e- mail address, service address, or other data specifically requested by the Biller at the time of activating electronic bills for that Biller.

Upon activation of the electronic bill feature, we may notify the Biller of your request to receive electronic billing information. The presentment of your first electronic bill may vary from Biller to Biller and may take up to sixty (60) days, depending on the billing cycle of each Biller. Additionally, the ability to receive a paper copy of your statement(s) is at the sole discretion of the Biller. While your electronic bill feature is being activated it is your responsibility to keep your Billing Accounts current. Each Biller reserves the right to accept or deny your request to receive electronic bills.

Your activation of the Bill Pay Service for a Biller is deemed to be your authorization for us to obtain bill data from the Biller on your behalf. For some Billers, you will be asked to provide us with your user name and password for that Biller. By providing us with such information, you authorize us to use the information to obtain your bill data.

We will present your electronic bills to you by notification within the Bill Pay Service. In addition, we may send an e-mail notification to the e-mail address listed for your Account. It is your sole responsibility to ensure that this information is accurate. In the event you do not receive notification, it is your sole responsibility to periodically log on to the Bill Pay Service and check on the delivery of new electronic bills. The time for notification may vary from Biller to Biller.

The Biller reserves the right to cancel the presentment of electronic bills at any time. You may cancel electronic bill presentment at any time. The timeframe for cancellation of your electronic bill presentment may vary from Biller to Biller. Depending on the billing cycle of each Biller, cancellation of electronic bill presentment may take up to sixty (60) days. We will not be responsible for paying any electronic bills that are already in process at the time of cancellation.

You agree to hold the Bank harmless should you fail to receive your electronic bill. You are responsible for ensuring timely payment of all bills. Copies of previously delivered bills must be requested from the Biller directly.

We are not responsible for the accuracy of your electronic bill(s). We only present the information we receive from the Biller. Any discrepancies or disputes regarding the accuracy of your electronic bill summary or detail must be addressed with the Biller directly.

SERVICE FEES AND ADDITIONAL CHARGES.

Any applicable fees will be charged regardless of whether the Bill Pay Service was used during the billing cycle. There may be a charge for additional transactions and other optional services as disclosed on the Terms and Conditions of Your Account and Fee Schedule that applies to your Bill Pay Account. You agree to pay such charges and authorize us to deduct the amount from your designated Bill Payment Account for these amounts and any additional charges that may be incurred by you. For Bill Pay Services for Consumers, the Bill Payment Account for service fees is the Account which the service or requested transaction impacts. For the Bill Pay Service for Businesses, the Bill Payment Account is the first Account enrolled in the Bill Pay Service. Any fees associated with your Accounts continue to apply. You agree that we may deduct from your Bill Payment Account any amount due, including for an amount due to a payment made under this Agreement.

FAILED OR RETURNED TRANSACTIONS.

In using the Bill Pay Service, you are requesting us to make payments for you from your Bill Payment Account. A Scheduled Payment will fail to result in a Bill Payment if any of the following occur:

Erroneous or incomplete information is provided by you, which prevents accurate and timely payment;

A Biller cannot or will not accept a payment delivered by us;

We suspect the payment of being fraudulent and have provided notification to you; or

We suspect that the Biller is a blocked entity under Office of Foreign Assets Control Sanctions.

We will notify you of each Scheduled Payment that does not result in a Bill Payment because of any of the reasons described above. If the Bill Payment does not occur due to any of items (2) through (5) above, we may request additional information regarding the failed Scheduled Payment. If you do not provide the information we need to resolve the failed Bill Payment within five (5) Business Days, the Scheduled Payment will be cancelled and funds will be re-credited to your Bill Payment Account.

If a Scheduled Payment does not result in a Bill Payment because (a) the Bill Payment Account from which the Scheduled Payment was scheduled has insufficient funds or (b) the Bill Pay Service could not retrieve the funds necessary to make the Scheduled Payment for any reason, then you acknowledge and agree that: (i) your Bill Pay Service will be CANCELLED for ALL of your Accounts; (ii) notice of such a failed Scheduled Payment as a result of (a) or (b) above will also constitute notice of the cancellation of your Bill Pay Service for ALL of your Accounts and any Scheduled Payments scheduled to be made after the failed Scheduled Payment; and (iii) all Scheduled Payments for ALL of your Accounts (including during the three (3) day period specified below) will be CANCELLED with no further notice to you and will not be made or initiated. This cancellation will remain in effect until we determine whether your Bill Pay Service will be restored.

During the time when your Bill Pay Service is cancelled as provided herein, it is your sole responsibility to provide for another means of payment for any cancelled Scheduled Payments.

You agree that we are not responsible or liable for the failure to process any Scheduled Payment for any of the reasons described above, including during any time that your Bill Pay Service is cancelled, whether or not there are sufficient funds in your Bill Payment Account(s) during such cancellation period. You also agree to indemnify and hold us harmless from any claims, liability, loss or damages resulting from our actions taken under this Section V.K. This provision amends and supersedes any conflicting provision of your Terms and Conditions of Your Account’s.

BILL PAY SCHEDULE.

A Properly Scheduled Payment is a Scheduled Payment that conforms with the terms and conditions of this Agreement and in which, at the time the payment was scheduled (i) there were sufficient funds in the Bill Payment Account to make the payment as requested; (ii) the Bill Payment Account and the Billing Account were open and in good standing, and (iii) the customer enrolled in the Bill Payment Service. The Bill Pay Service will not apply to any Properly Scheduled Payment that is late (a) as the result of any reason identified in Subsection J (Failed or Returned Transactions) or Subsection N (Delayed and Returned Payments; or (b) if you have failed to promptly provide us notice of the late payment within two (2) Business Days after your discovery of the late payment received by your Biller

SERVICE TERMINATION AND CANCELLATION OF PAYMENTS.

You may terminate your Bill Pay Service at any time. Any Scheduled Payment(s) scheduled to occur before the cancellation date will be completed. All Scheduled Payments, including Recurring Payments, scheduled to occur after the cancellation date of your Bill Pay Service will not be processed. We may terminate your Bill Pay Service at any time. I f any of your Bill Payment Accounts are closed, we will automatically cancel your Bill Pay Service for the applicable Bill Payment Accounts and no Scheduled Payments, including Recurring Payments, will be made by us from any of the closed Bill Payment Accounts. If the primary Account linked to your Bill Payment Account is closed, you made add an additional account to fund you Bill Payments or we will automatically cancel your Bill Pay Service for all your Bill Payment Accounts and no Scheduled Payments, including Recurring Payments, will be made by us from any of your Bill Payment Accounts. You must make other arrangements to make these payments.

BILLER AND PAYMENT LIMITATIONS.

Bill Pay Services will be monitored for compliance with laws and regulations governing currency transactions and money laundering. We reserve the right to refuse to pay any Biller to whom you may direct a payment or refuse any Scheduled Payment. We will notify you promptly if we refuse to pay a Biller designated by you or refuse to make a Scheduled Payment. This notification is not required if you attempt to make a prohibited payment under this Agreement.

DELAYED AND RETURNED PAYMENTS.

You will be notified if a delay occurs in the processing of your Scheduled Payment. You may be instructed to call Customer Service or we may call you if we need more information in order to process the transaction.

You understand that Billers and/or the United States Postal Service may return payments to us for various reasons such as, but not limited to, Biller’s forwarding address expired; Billing Account number is not valid; Biller is unable to locate Billing Account; or Billing Account is paid in full. We will research and correct the returned payment and return it to your Biller, or void the payment and credit your Bill Payment Account.

ADDRESS OR OTHER CHANGES.

All changes made are effective immediately for scheduled and future payments paid from the updated Bill Payment Account Information. We are not responsible for any payment processing errors or fees incurred if you do not provide accurate Billing Account or contact information.

LIABILITY FOR UNAUTHORIZED TRANSFERS OR PAYMENTS.

You are required to promptly provide notice to us of any unauthorized transfer at 1-815-385-3000 or by sending an email message through our secure messaging system located within Consumer e-Banking and Business e-Banking. When you give another party your Security Credentials, you are authorizing that party to use the Bill Pay Service and you are responsible for all payments that party performs while using your Security Credentials, even those you did not intend or want performed. If you are a Consumer customer, your liability for unauthorized electronic transfers or payments is described in your Deposit Terms and Conditions. Please note that if the Biller you scheduled a payment to is an individual, if the Biller does not appear on a list of pre-approved Billers when you input the Biller’s information within the Bill Pay Service, or if we notify you the payment will be made by check, we will make Bill Payments by check to those Billers

ADDITIONAL TERMS FOR BUSINESS ACCOUNTS.

Linking Multiple Accounts. You may use the Bill Pay Service to access Business Accounts. These Business Accounts include accounts of affiliated, subsidiary, or non-affiliated businesses bearing the same Tax Identification Number (TIN).

Information Authorization. Your enrollment in the Business e-Banking Bill Pay Service may not be fulfilled if we cannot verify your identity or other necessary information.

Enhanced Remittance. You may use the Business e-Banking Bill Pay Service to transmit additional detail related to the payment to the Biller such as invoice numbers, credit memo detail and dollar amounts by following the directions within the Bill Pay Service.

Liability for Transfers or Payments. We will have no liability to you for any errors or losses you sustain in using the Bill Pay Service except where we fail to exercise ordinary care in processing any transaction. The Bank is liable only for those unauthorized transfers that occur after you have provided notice to us and we have had a reasonable opportunity to act. We also are not liable for any failure to provide any service if the Account(s) involved is no longer linked for the Bill Pay Service. Our liability, if any, is limited to the amount of any funds improperly transferred from your Bill Payment Account less any amount that would have been lost even with the exercise of ordinary care.

PERSONAL FINANCE MANAGER SERVICE.

The Personal Finance Manager Service is a personal financial information management service that allows you to aggregate your account information by consolidating it into a single location (e.g. credit cards, investments, or accounts with institutions).

YOUR ACCOUNTS LINKED THROUGH PERSONAL FINANCE MANAGER SERVICE.

You represent, warrant and agree that (i) you are the sole legal and beneficial owner of each account with respect to which you request the Bank to provide the Personal Finance Manager Service and/or (ii) if you are not the sole legal and beneficial owner of any account with respect to which you request Bank to provide the Personal Finance Manager Service, including, without limitation, accounts held in joint ownership or in trust, you have the legal authority to include the account in the Personal Finance Manager Service and to share Account Information with respect to the account. With respect to any beneficial interest in a trust or other fiduciary account for which Account Information is provided at your request, you hereby expressly consent to delivery by the fiduciary of all Account Information which you are eligible to receive to the Bank.

DESCRIPTION OF PERSONAL FINANCE MANAGER SERVICE.

The Personal Finance Manager Service is an information management service that allows you to consolidate and manage selected information from various websites. The Personal Finance Manager Service allows you to consolidate, retrieve, view and maintain Account Information stored. After registering for the Personal Finance Manager Service, you will provide us information about the accounts you wish to aggregate. The Personal Finance Manager Service periodically obtains your Account Information from us and third party websites based on the information you have previously provided to us. The Bank and the third party vendor that provides the Personal Finance Manager Service do not have access to the username and passwords you use on other third party websites. You must provide us such username and passwords or other Security Credentials for this service.

THIRD PARTY INFORMATION, CONTENT, PRODUCTS AND SERVICES.

Other than Account Information, all other information available through the Personal Finance Manager Service is provided by third parties. We are not responsible for the products, services, and accuracy of information at third party sites or viewed through our Personal Finance Manager Service. You acknowledge that we do not pre-screen content, but that we will have the right (but not the obligation) in our sole discretion to refuse, edit, move or remove any content that is available through the Personal Finance Manager Service.

THIRD PARTY ACCOUNTS.

By using the Personal Finance Manager Service to access a third party website you have designated, you authorize us and our providers to access the third party websites and accounts you designate to retrieve Third Party Account Information on your behalf, and you appoint us as your agent for this limited purpose. You represent that you are a legal owner of the accounts at third party websites which you include in the Personal Finance Manager Service and that you have the authority to (i) designate us as your agent, (ii) use the Personal Finance Manager Service and (iii) give us your passwords, usernames, and all other information you provide. YOU AGREE AND ACKNOWLEDGE THAT WHEN WE ACCESS AND RETRIEVE INFORMATION FROM A THIRD PARTY WEBSITE, WE ACT AS YOUR AGENTS, AND NOT THE AGENTS OR ON BEHALF OF THE THIRD PARTY. Transactions and inquiries you initiate at such a site are not made through, and we have no responsibility for such transactions. You agree to comply with the terms and conditions of those accounts. If you have a dispute or question about any transaction on such site, you agree to direct these to the account provider. Third party websites are entitled to rely on the above authorization granted by you. Balances shown on the Personal Finance Manager Service reflect the most recent refresh and may not be accurate if a refresh was not successfully completed or the information obtained during the refresh from the third party is otherwise not accurate or current.

MOBILE CHECK DEPOSIT SERVICE.

DESCRIPTION OF SERVICE.

Our Mobile Check Deposit service offered through Consumer e-Banking and Business e-Banking allows you to make deposits of an electronic image of a check to your eligible checking, or savings accounts at the Bank by capturing an electronic image of the item with the capture device (such as a camera) on your Mobile Device and submitting images and information about the item to us for processing.

ELIGIBLE CHECKS.

You agree that you will not use the Mobile Check Deposit Service to deposit any of the following Items:

Checks that have already been presented to, or paid by, another person, company or depository institution;

Checks drawn on a financial institution located outside the United States; or

Checks containing obvious alteration to any of the fields on the front of the Check, or which you know or suspect, or should know or suspect, are fraudulent; or Items prohibited by our current procedures relating to the Mobile Check Deposit Service or which are otherwise not acceptable under the terms of your applicable checking, or savings account and related agreement with us. You can find information about our current procedures through the Frequently Asked Questions for the Mobile Check Deposit Service available on our website at: https://www.mchenrysavings.com/

CHECK IMAGE QUALITY.

The image of a Check transmitted using the Mobile Check Deposit Service must be legible and clear. It must not be altered. It must capture all pertinent information from both sides of the Item. Image quality must comply with industry requirements established and updated by the American National Standards Institute (ANSI), the Board of Governors of the Federal Reserve System and any other applicable regulatory agency.

ENDORSMENT OF CHECKS.

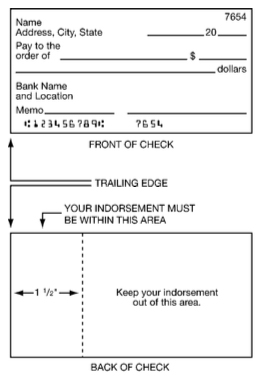

You must sign each Check to be submitted using the Mobile Check Deposit Service with a restrictive endorsement reading “For Mobile Deposit Only at McHenry Savings Bank” or a restrictive endorsement in materially the same form that would prevent deposit, presentment, and negotiation of the Check after submission via the Mobile Check Deposit Service.

PROCESSING TIME AND AVAILABILITY OF FUNDS.

If we receive the image of a Check for deposit on or before 4:00 p.m. Central Time (CT) on a Business Day, we will consider that day the day of deposit. If we receive the image of a Check for deposit after 4:00 p.m. CT or on a weekend or on a non-Business Day, we will consider the next Business Day as the day of deposit. For Checks deposited into checking accounts, we will adhere to the legal requirements on funds availability.

DISPOSAL OF TRANSMITTED CHECKS.

After 15 Business Days following the deposit using the Mobile Check Deposit Service, if you have verified that the funds have been credited to your Account, you agree to mark the item as "VOID" and properly dispose of it to ensure it is not presented for deposit again. You agree to safeguard and keep the original Check for one year after you have transmitted the Item. If you fail to follow these procedures and you or any third party cashes or re-deposits the Item, you may be liable to us for the amount of the Check.

RESTRICTIONS AND LIMITATIONS ON CHECKS.

Your use of the Mobile Check Deposit Service will be subject to the following restrictions and limitations:

Only Checks that originated as paper Items and no third party or electronic checks may be deposited using Mobile Check Deposit Service.

The maximum number of Checks that may be deposited in one day is 5.

There is a maximum deposit limit of $2,500.00 within three consecutive days.

The maximum number of Checks that may be deposited in a three consecutive day period is 5.

DEPOSITOR AGREEMENTS.

You agree that after you submit a Check for deposit using the Mobile Check Deposit Service, you will not re- deposit or otherwise transfer or negotiate the original Check. You further agree not to deposit Checks into your Account unless you have authority to do so. After you submit a Check for deposit you are solely responsible for the storage or destruction of the original Check. The electronic image of the Check will become the legal representation of the Check for all purposes, and you agree that any image we receive accurately and legibly represents all of the information on the front and back of the original Check as originally drawn.

FUNDS AVAILABILITY.

Funds from electronic check deposits are generally made available within the timeframes set forth in the Bank’s funds availability policy applicable to the Account. The Bank, however, reserves the right to make such deposits available at its discretion.

ELIGIBILITY.

You must meet our eligibility requirements in order to use the Mobile Check Deposit Service. These eligibility requirements include being a Consumer e-Banking or Business e-Banking customer of the Bank who has had a savings account for more than 30 days in good standing. We may change the eligibility requirements from time to time in our sole discretion.

ERRORS.

You agree to notify us of any suspected errors related to your deposit made with the Mobile Check Deposit Service immediately and no later than 30 days after the applicable account statement is provided, or as otherwise specified in your Terms and Conditions of your Account with us, found at https://www.mchenrysavings.com/

REPORTING UNAUTHORIZED TRANSACTIONS.

If you believe someone may attempt to use or has used the Mobile Check Deposit Service in connection with your Account without your permission, or that any other unauthorized use or security breach has occurred, call us immediately at 1-815-385-3000 or write us at McHenry Savings Bank, 353 Bank Dr., McHenry, IL. 60050. Telephoning is the best way to minimize your losses for any error or unauthorized transaction.

CUSTOMER SERVICE.

If you have any questions about the Mobile Check Deposit Service, email customerservice@mchenrysavings.com or call as at 1-815-385-3000.

TERMINATION.

If your Account with the Bank is terminated for any reason or no reason, you agree: (a) to continue to be bound by this Agreement, (b) to immediately stop using the Mobile Check Deposit Service, (c) that the license provided under this Agreement shall end, and (d) that we shall not be liable to you or any third party for termination of access to the Mobile Check Deposit Service. You may request at any time that we terminate your access to the Mobile Check Deposit Service. We may terminate your access to the Mobile Check Deposit Service and close your Account(s) for any reason or no reason at any time upon notice to you, including if we believe you are in breach of this Agreement or your Terms and Conditions of Your Account. Account with us, found at https://www.mchenrysavings.com/

INDEMNIFICATION.

Except as otherwise provided under applicable law, you agree to indemnify, defend and hold us harmless from and against any and all claims, losses, liability, cost and expenses (including reasonable attorneys’ fees) arising from your use of the Mobile Check Deposit Service, the use of a telephone or mobile phone number, email address, or other delivery location that is not your own, or your violation of applicable federal, state or local law, regulation or ordinance. Your obligation under this paragraph shall survive termination of the Mobile Check Deposit Service and this Agreement.

GOVERNING LAW.